The moments after a car crash are disorienting. Amid the confusion and shock, the actions you take can significantly influence the outcome of your insurance claim. Protecting your health and your right to fair compensation begins right at the scene, long before you ever speak to an adjuster.

Immediate Actions at the Scene of the Crash

In the immediate aftermath of a collision, your first priority is always safety. Before you think about insurance or legal matters, you must secure the scene to prevent further harm. Once everyone is safe, your focus can shift to gathering the essential information that will form the foundation of your claim.

Follow these steps methodically:

- Prioritize Safety Above All Else. First, check yourself and your passengers for injuries. If your vehicle is in a dangerous spot and can be moved, pull it to the side of the road. Turn on your hazard lights immediately. This simple action alerts other drivers and helps prevent a secondary, more dangerous accident.

- Call 911 Without Hesitation. A police report is an official, unbiased record of the incident. Insurance companies rely heavily on this document. Even if the accident seems minor, a police report provides critical details. Paramedics should also evaluate everyone involved. Adrenaline can easily mask injuries that may become apparent hours later.

- Exchange Key Information, Not Opinions. You need to collect specific details from the other driver: their full name, address, phone number, insurance company, and policy number. Also, get their driver’s license and license plate numbers. It is critical to avoid apologies or any discussion of fault. Simply state the facts. Saying “I’m so sorry” can be misinterpreted as an admission of guilt.

- Document Everything Visually. Your smartphone is your most powerful tool at the scene. Take photos and videos of everything. Capture the damage to all vehicles from different angles, any skid marks on the road, nearby traffic signals, and the overall weather conditions. If there are witnesses, ask for their names and phone numbers. Their perspective can be invaluable.

Building Your Case with Thorough Documentation

Once you have left the scene, the process of protecting your claim shifts to meticulous record keeping. The initial evidence you gathered is a great start, but the documentation you compile in the following days and weeks is what truly demonstrates the full extent of your damages. This is where a scattered collection of notes becomes a solid, undeniable case file.

Seek Prompt Medical Attention

Adrenaline is powerful and can hide serious conditions. What feels like minor soreness could be a more significant injury. Seeking a medical evaluation right away creates an official record that links your injuries directly to the crash. As the Centers for Disease Control and Prevention (CDC) highlights, symptoms of serious injuries like traumatic brain injury may not appear for hours or days, making an immediate medical check-up essential for both your health and your claim.

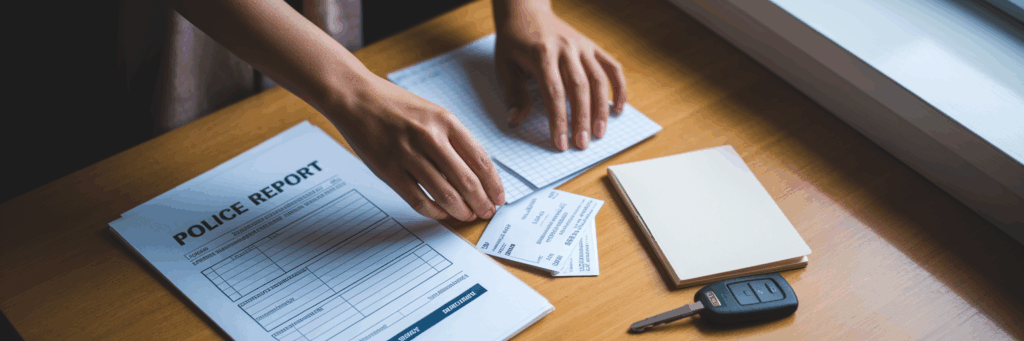

Create a Centralized Claim File

Get a physical folder or create a dedicated digital directory on your computer. This is where every single document related to the accident will live. Store the police report, medical bills, repair estimates, and any correspondence with insurance companies. An organized file not only keeps you in control but also shows the insurer that you are diligent and serious about your claim. A strong case file is the foundation of any successful claim, a principle that guides experienced car accident lawyers.

Maintain a Detailed Personal Journal

This is one of the most effective car accident compensation tips that is often overlooked. Bills and receipts show financial costs, but they don’t capture your human experience. Start a journal to track your daily pain levels on a scale of 1 to 10, your emotional state, any sleep disruptions, and specific daily activities you can no longer perform. This detailed narrative is powerful evidence for a pain and suffering claim, providing context that a medical bill never could.

| Document Type | Why It’s Important | How to Obtain It |

|---|---|---|

| Police Report | Provides an official, third-party account of the accident. | Request a copy from the responding police department. |

| Medical Records & Bills | Directly links your injuries to the crash and proves costs. | Request from your doctor, hospital, and physical therapist. |

| Repair Estimates | Establishes the full value of your vehicle damage. | Get at least two estimates from reputable auto body shops. |

| Proof of Lost Wages | Quantifies income lost due to inability to work. | Obtain a letter from your employer detailing missed time and pay rate. |

| Personal Injury Journal | Documents pain, suffering, and impact on daily life. | Maintain a daily notebook or digital log. |

| Photos and Videos | Offers indisputable visual evidence of the scene and damages. | Use your smartphone at the scene and during recovery. |

Critical Mistakes That Can Weaken Your Claim

After an accident, you are in a vulnerable position. Insurance companies understand this, and certain missteps can give them the leverage they need to reduce or deny your compensation. Knowing the common mistakes to avoid after car accident is just as important as knowing what to do. These principles apply not just to vehicle collisions but to a wide range of personal injury practice areas.

- Admitting Fault: Never admit fault, even partially. A simple “I’m sorry” can be used against you as an admission of liability. Stick to the objective facts of what happened without assigning blame.

- Giving a Recorded Statement Too Soon: The other driver’s insurance company will likely call you quickly and ask for a recorded statement. You are not obligated to provide one. These calls are often used to find inconsistencies in your story or to get you to downplay your injuries. Politely decline until you have had time to assess your situation.

- Posting on Social Media: Assume that insurance investigators will look at your social media profiles. A photo of you at a friend’s barbecue or on a short walk could be used to argue that your injuries are not as severe as you claim. It is best to refrain from posting until your claim is resolved.

- Accepting the First Settlement Offer: The initial offer from an insurance company is almost always a lowball figure. They hope you will accept it to close the case quickly and cheaply. Never accept an offer until you know the full extent of your medical treatment, future needs, and lost income.

Navigating Communications with Insurance Companies

Once you file a claim, you will begin interacting with an insurance adjuster. How you manage these conversations is critical. This is not just about avoiding errors; it is about strategically controlling the narrative to protect your interests. Learning how to deal with insurance adjuster communications can prevent them from dictating the value of your claim.

Understand the Adjuster’s Role

The insurance adjuster may seem friendly and helpful, but it is essential to remember their primary job: to protect their company’s financial interests. This means settling your claim for the lowest amount possible. They are trained negotiators and are not your advocate. Approaching every conversation with this understanding will help you remain objective and firm.

Control the Flow of Information

Whenever possible, communicate in writing, such as through email. This creates a clear record of all interactions. If you must speak on the phone, keep the conversation brief and stick to the facts. Do not offer any information they do not specifically request. Be especially wary of signing broad medical authorization forms. These can give the insurer access to your entire medical history, which they may use to argue that your injuries were caused by a pre-existing condition.

Keep a Detailed Communication Log

Just as you keep a journal for your injuries, you should keep a log for all communications with the insurer. For every call or email, note the date, time, the name of the person you spoke with, and a brief summary of the conversation. This log is invaluable for holding the adjuster accountable for what they say and for countering any delay tactics.

If you find the adjuster is using delay tactics or pressuring you for a statement, it may be time to seek professional guidance. You can contact us for a free, no-obligation consultation to discuss your case.

Knowing When to Consult a Personal Injury Attorney

Many straightforward claims can be handled without legal help. However, certain situations are complex and present significant risks to your financial recovery. Recognizing these red flags is key to knowing when to hire accident attorney. Doing so is not an aggressive move; it is a strategic decision to level the playing field and maximize car accident settlement potential.

Consider seeking legal advice if you encounter any of these situations:

- Your injuries are serious, long-term, or permanent.

- The insurance company is disputing who was at fault for the crash.

- The settlement offer is too low to cover your medical bills and lost wages.

- The insurer is delaying your claim or has denied it without a clear reason.

A dedicated personal injury lawyer does more than just file paperwork. They take over all communications with the insurance company, gather the necessary evidence, and consult with experts to accurately calculate the full value of your claim. This includes not only your medical bills and lost income but also non-economic damages like pain and suffering.

Many people hesitate to call an attorney because they worry about the cost. However, most personal injury lawyers work on a contingency fee basis. This means you pay no upfront fees. The attorney is only paid a percentage of the settlement they win for you. If you do not win your case, you owe no attorney fees. Finally, remember that every state has a strict statute of limitations for filing a claim. As noted by Cornell Law School’s Legal Information Institute, this is a deadline that, if missed, can permanently bar you from recovering compensation. Acting promptly is essential to protect your rights.